Posted on Apr 16, 2015

")

Tactical and Strategic Investing: Part III of IV

7.11K

26

15

7

7

0

In Part I, I explained how to think about “Strategic Investing” – specifically, where you want to be financially in the next 10-40 years and in Part II, I explained how you should think tactically to invest strategically. Now in Part III, I’m going to explain how to diversify your investments!

I want you to keep in mind: I’m NOT a stockbroker or investment account manager of any sort. The advice I’m giving here is based on well-known principles of investing, but in my opinion, any investment manager is going to tell you the same thing: diversify.

One of the key concepts in investing, especially for the long term, is “diversification”. This is a big word that we think we understand, but often don’t.

In a military battle, you want to spread your forces out far enough to protect an area, but not so much that the enemy can just get inside by finding the gaps.

With investing, you want to do the same thing - spread your money out, or diversify, but not so much that it becomes problematic to retrieve it when you need it. There are a two of reasons for this:

- First, by spreading your money out, you are ensuring that even if one investment fails, you have others that are succeeding and generating money (and when you retire for good, providing income).

- Second, by spreading your money out into a retirement account, some mutual funds, some precious metals, and maybe some stocks and bonds, you are creating multiple sources of cash later on.

This leads to the next question: what should you diversify in? I can’t give you specific guidance because everyone has their own ideas, but in general, you should invest in your IRA/401K retirement accounts first (preferably some sort of mutual funds), next into regular mutual funds, then into some sort of precious metals, and finally maybe some stocks and bonds. Again, note that this is how I believe investments should be managed but your situation and beliefs may be different. The key though, no matter what strategy you adopt, is to diversify and spread your investments out across several investment sources.

Keep in mind that when you’re investing into an IRA, you probably want to put as much of your investment money as possible into a “Roth-IRA” because when you do, you pay your taxes at the front as you invest your money. This means that no matter how much money your Roth-IRA generates, you don’t have to pay taxes on it when you withdraw it. There are limits to how much you can contribute to a Roth-IRA, and there are income-based restrictions as well, so make sure you do a little research before you invest in one. In fact, you should do research anyway!

The last question is how much should I invest? Well, most advisors recommend about 15% of your income, however, it really depends on how much you can afford. If you’re able to put more in then do so, but if you can only put 5% right now, then put 5%. At a minimum, I would put at least $50-$100 per pay check if at all possible and then, when you have extra cash that you don’t need at the end of a pay period, put that in as well. This is probably the most important thing you need to do: no matter what, you need to invest something – even if it’s only $20 a week, put it into an investment. If you can’t do even that, chances are you will never get to a point where you can retire with a couple of million in the bank!

In Part IV, I’ll cover some specific situations to consider when it comes to investing.

Comment below or start the conversation here and connect within the military community.

I want you to keep in mind: I’m NOT a stockbroker or investment account manager of any sort. The advice I’m giving here is based on well-known principles of investing, but in my opinion, any investment manager is going to tell you the same thing: diversify.

One of the key concepts in investing, especially for the long term, is “diversification”. This is a big word that we think we understand, but often don’t.

In a military battle, you want to spread your forces out far enough to protect an area, but not so much that the enemy can just get inside by finding the gaps.

With investing, you want to do the same thing - spread your money out, or diversify, but not so much that it becomes problematic to retrieve it when you need it. There are a two of reasons for this:

- First, by spreading your money out, you are ensuring that even if one investment fails, you have others that are succeeding and generating money (and when you retire for good, providing income).

- Second, by spreading your money out into a retirement account, some mutual funds, some precious metals, and maybe some stocks and bonds, you are creating multiple sources of cash later on.

This leads to the next question: what should you diversify in? I can’t give you specific guidance because everyone has their own ideas, but in general, you should invest in your IRA/401K retirement accounts first (preferably some sort of mutual funds), next into regular mutual funds, then into some sort of precious metals, and finally maybe some stocks and bonds. Again, note that this is how I believe investments should be managed but your situation and beliefs may be different. The key though, no matter what strategy you adopt, is to diversify and spread your investments out across several investment sources.

Keep in mind that when you’re investing into an IRA, you probably want to put as much of your investment money as possible into a “Roth-IRA” because when you do, you pay your taxes at the front as you invest your money. This means that no matter how much money your Roth-IRA generates, you don’t have to pay taxes on it when you withdraw it. There are limits to how much you can contribute to a Roth-IRA, and there are income-based restrictions as well, so make sure you do a little research before you invest in one. In fact, you should do research anyway!

The last question is how much should I invest? Well, most advisors recommend about 15% of your income, however, it really depends on how much you can afford. If you’re able to put more in then do so, but if you can only put 5% right now, then put 5%. At a minimum, I would put at least $50-$100 per pay check if at all possible and then, when you have extra cash that you don’t need at the end of a pay period, put that in as well. This is probably the most important thing you need to do: no matter what, you need to invest something – even if it’s only $20 a week, put it into an investment. If you can’t do even that, chances are you will never get to a point where you can retire with a couple of million in the bank!

In Part IV, I’ll cover some specific situations to consider when it comes to investing.

Comment below or start the conversation here and connect within the military community.

Posted >1 y ago

Responses: 6

4

4

0

The most important thing is not where you invest, but that you invest. Start young, make it a habit, allow it to compound...

(4)

(0)

CAPT Stu Merrill

Congrats on your dedicated 33% based on your current living and family conditions - very impressive!

(0)

(0)

3

3

0

One investment not to forget is land. There is only so much of it. I've bought land and sold it some years later and made a good profit. Just remember you need to invest money you DON'T need as this is a long term investment. What ever you invest in, it's not how much you invest at once, but how long you do. I'd watch out for stocks and such unless you can really watch that stuff.

(3)

(0)

SFC (Join to see)

SGM Mikel Dawson Land can be a good investment. However, you have to be careful. If you buy the wrong piece of property, you could wind up with something you can't get rid of. My rule is: If I can live on the land, and it's accessible, or could be accessible in 10-15 years, then I'd consider it. If it's so remote that there's not going to be any chance of it ever being reachable in my lifetime, then I wouldn't.

Also, unless you can afford to pay cash outright, you're going to owe the bank - which means you will pay interest on that loan. So unless the land is increasing in value at an exceptional rate, or you can get the loan paid off quickly, you're going to need to do some serious math to figure out if the interest you're going to pay for the loan, is going to be less than what you stand to gain when you sell the land. If what you stand to gain isn't going to be more than a few % after you figure out the interest on the loan, I'd pass.

Also, unless you can afford to pay cash outright, you're going to owe the bank - which means you will pay interest on that loan. So unless the land is increasing in value at an exceptional rate, or you can get the loan paid off quickly, you're going to need to do some serious math to figure out if the interest you're going to pay for the loan, is going to be less than what you stand to gain when you sell the land. If what you stand to gain isn't going to be more than a few % after you figure out the interest on the loan, I'd pass.

(0)

(0)

SGM Mikel Dawson

I've made two land investments. Sold one for twice what I paid for it. The other I've been offered half again as much as I paid. I'm sitting on the one. It's a long term investment. Bought it 25yrs ago, so like you say, one's got to be careful, but if done right can pay off.

(1)

(0)

3

3

0

I'm a coordinator for Dave Ramsey's Financial Peace University. He continuously reiterates diversifying investments. For my 401K, I have 25% Small cap, 25% mid cap, 25% large cap, and 25% in international funds.

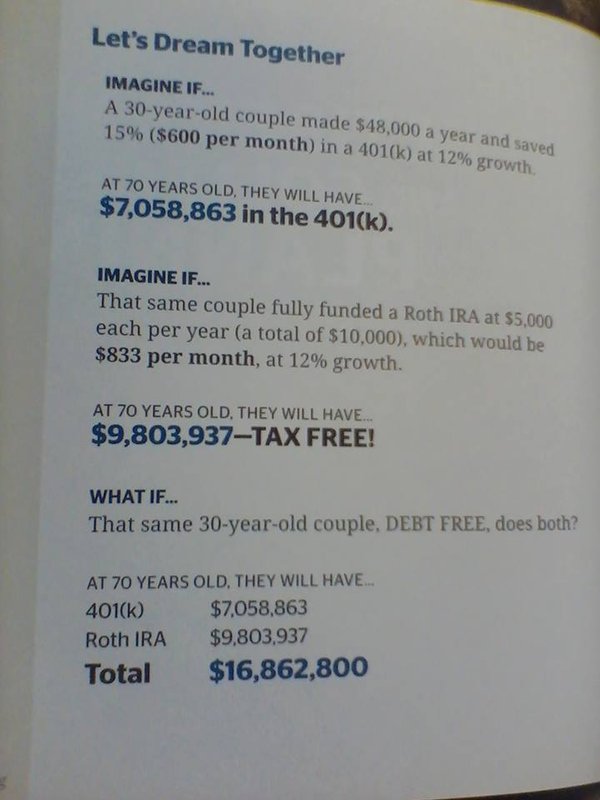

If you think your money doesn't amount to much, think again. compound interest is definitely your friend. Check out the picture from our FPU class below. $600 a month - or only $150 per week. Find a way to make it happen. Cut the lattes, cut the cigarettes, cut the cable (netflix is a great thing) etc... and fund your future...

If you think your money doesn't amount to much, think again. compound interest is definitely your friend. Check out the picture from our FPU class below. $600 a month - or only $150 per week. Find a way to make it happen. Cut the lattes, cut the cigarettes, cut the cable (netflix is a great thing) etc... and fund your future...

(3)

(0)

Read This Next