Posted on Dec 11, 2015

")

Is the SGLI enough to give you true financial security?

20.6K

17

16

1

1

0

http://archive.armytimes.com/article/20120121/BENEFITS08/201210303/It-pays-enough-life-insurance-Policies-beyond-SGLI-can-spell-financial-security

I can help make this your reality as well, don't wait until it's too late..hooah?

I can help make this your reality as well, don't wait until it's too late..hooah?

Posted 9 y ago

Responses: 5

4

4

0

No SGLI is not enough to give your beneficiaries true financial stability 1LT (Join to see).

I recommend you but some type of permanent insurance with no frills while you are young when it costs less and get a rider which allow you to purchase additional policies, allow to to purchase policies for future children in case.

Start at IRA or Roth IRA and increase the amount you contribute to it whenever you get a pay raise - that way you do not notice any loss in income and increase what goes into your retirement. I recommend you invest in mutual funds instead of individual stocks. Ask around and find a low cost or no cost organization which will help you purchase insurance and start an IRA.

I recommend you but some type of permanent insurance with no frills while you are young when it costs less and get a rider which allow you to purchase additional policies, allow to to purchase policies for future children in case.

Start at IRA or Roth IRA and increase the amount you contribute to it whenever you get a pay raise - that way you do not notice any loss in income and increase what goes into your retirement. I recommend you invest in mutual funds instead of individual stocks. Ask around and find a low cost or no cost organization which will help you purchase insurance and start an IRA.

(4)

(0)

1LT (Join to see)

Hooah Sir, my firm is no-fee based and we hit on permanent life insurance at a young age, contributing to Roth IRA's while investing in low fee mutual funds exactly like you said. Thank you for your contribution.

(1)

(0)

SFC Michael Jackson, MBA

LTC Stephen F. is 100% correct. Excellent advice. Anyone not taking his advice is making a HUGE life mistake. only thing i can possibly add is start NOW, Don't wait any longer

(1)

(0)

0

0

0

Take note that SGLI stands for Soldier's Group Life Insurance. That means that you are only eligible to have it as long as you are serving. When you separate from service, you have a very narrow window (120 days) in which you can switch it over to VGLI (Veteran's Group Life Insurance). At this point, you start paying the premiums, based on your age category. Premium age brackets are 5 years, so you can expect a premium increase as you get older. It is TERM insurance.

There are some companies (a very short list compared to the 1000's of insurance companies out there) who will convert VGLI to a whole life policy under their company's products without considering current health conditions or insurability. Most insurance agents don't even know about SGLI/VGLI conversions because very, very few companies will do it and if they do, it is usually a single product that it converts to. Also, because there's no underwriting to do the conversion, agents don't get a commission for putting that policy into force unless the client adds riders or additional things to the policy.

Btw, any question regarding financial security has no universal right answer because every answer depends on the individual's circumstances and requirements for their household and future plans.

There are some companies (a very short list compared to the 1000's of insurance companies out there) who will convert VGLI to a whole life policy under their company's products without considering current health conditions or insurability. Most insurance agents don't even know about SGLI/VGLI conversions because very, very few companies will do it and if they do, it is usually a single product that it converts to. Also, because there's no underwriting to do the conversion, agents don't get a commission for putting that policy into force unless the client adds riders or additional things to the policy.

Btw, any question regarding financial security has no universal right answer because every answer depends on the individual's circumstances and requirements for their household and future plans.

(0)

(0)

0

0

0

How much one should insure oneself for is a personal item. The answer is vastly different for each situation. There are really no simple answers.

Obviously if one knows that death is coming soon get all you can. Problem is you will find you can not get any.

I sold life insurance and after a single trip to the doctor I could not even sell myself any.

Obviously if one knows that death is coming soon get all you can. Problem is you will find you can not get any.

I sold life insurance and after a single trip to the doctor I could not even sell myself any.

(0)

(0)

Capt (Join to see)

1LT (Join to see) - I was diagnosed with diabetes. Therefore no longer insurable with the company I worked for.

(0)

(0)

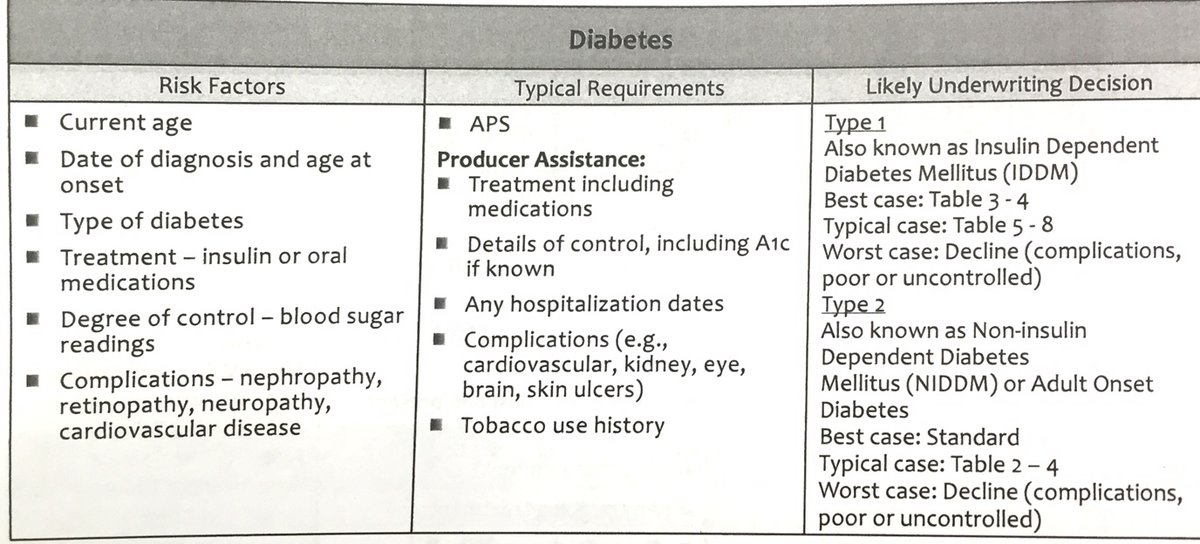

1LT (Join to see)

Capt (Join to see) - Here's the underwriting guidelines for Penn Mutual, you may be uninsurable with that company but it doesn't mean you would be with Penn Mutual. I've placed multiple cases at preferred and standard ratings for clients that have had cancer in the past.

(0)

(0)

Capt (Join to see)

1LT (Join to see) - Thanks, but I have progressed to non insurable by your chart. Five shots of insulin a day. Plus at my age insurance is seldom affordable.

(0)

(0)

Read This Next